EU Travel Rule Compliance for Crypto: What Zero Threshold Means for Businesses

May, 18 2025

May, 18 2025

EU Travel Rule Compliance Checker

How This Tool Works

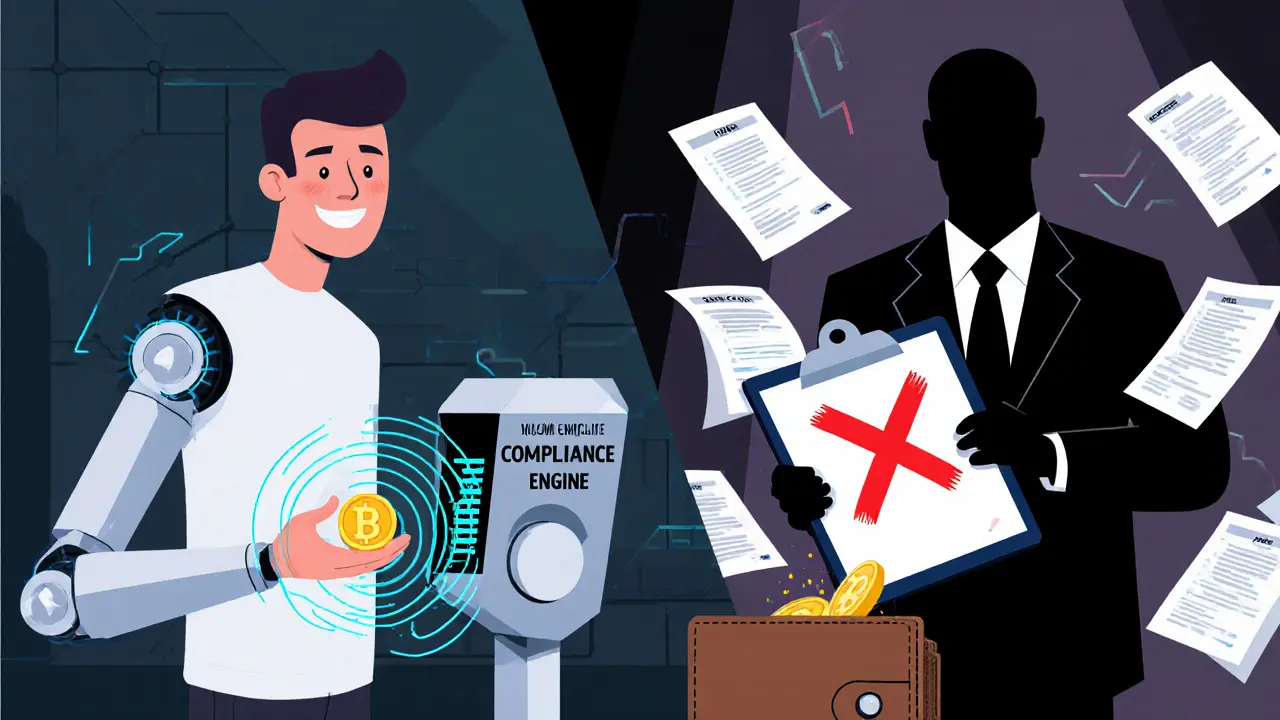

The EU Travel Rule applies to every transaction between regulated Crypto Asset Service Providers (CASPs), regardless of amount. This tool helps you determine if your transaction requires full identity data exchange.

Key Facts: No minimum threshold. Applies to all transactions (even €0.01). Data must include full names, account numbers, and physical addresses for both sender and recipient.

Full identity data exchange required between regulated CASPs.

Why This Matters

This rule affects all crypto businesses operating in the EU. If you're sending to a non-compliant provider, your transaction may be blocked, delayed, or flagged as high-risk.

Remember: The EU Travel Rule applies even for transactions as small as €0.01 when both parties are regulated CASPs.

On December 30, 2024, every crypto transaction in the European Union changed forever. Not because of a price crash or a new coin launch, but because of a rule that applies even when you send one euro. The EU’s Travel Rule, now fully in force, requires crypto businesses to collect and share full identity details for every single transfer - no matter how small. There’s no minimum. No exception. Not even for €0.01.

What Exactly Is the EU Travel Rule?

The EU Travel Rule isn’t new. It’s part of Regulation (EU) 2023/1113 and Regulation (EU) 2023/1114 (MiCA), passed in April 2023 and生效 on June 29, 2023. But the deadline that mattered - December 30, 2024 - is when it became real for every crypto asset service provider (CASP) operating in the EU. This means exchanges, wallet providers, and any firm handling crypto on behalf of users must now collect and transmit the sender’s and recipient’s full names, account numbers, and physical addresses for every transaction, regardless of value.This is the strictest version of the Travel Rule in the world. The FATF, the global anti-money laundering watchdog, originally suggested a $1,000 threshold. The U.S. still uses $3,000. The EU went further: zero. Every transfer. Every time. Even if you’re paying a freelancer €5 for a logo. Even if you’re sending €2 to a friend. If it goes through a regulated CASP, it’s tracked.

Why Does This Matter to You?

If you run a crypto business in the EU, this rule changes your entire operational model. You can’t just rely on basic KYC anymore. You now need systems that:- Automatically capture sender and beneficiary data for every transaction

- Verify the identity of the receiving CASP before sending funds

- Store this data securely for at least five years

- Exchange it in real-time using approved messaging protocols

- Handle cases where the other side doesn’t comply

It’s not optional. If you don’t have this in place, you’re breaking EU law. Regulators in Germany, France, and the Netherlands have already started audits. Fines can reach up to 5% of annual turnover or €5 million - whichever is higher. And it’s not just about money. If your platform is flagged for non-compliance, other CASPs will cut you off. No one wants to risk receiving funds from a non-compliant partner.

What Happens When Data Is Missing?

This is where things get messy. Not every crypto business in the world follows the EU’s rules. If you’re sending €100 to a wallet outside the EU - say, in Singapore or Nigeria - and that wallet isn’t regulated under MiCA, the receiving CASP doesn’t have to send back full data. So what does your EU-based exchange do?The regulation gives you three choices: accept, reject, or suspend. But you can’t just guess. You need a risk-based system. If the transaction comes from a high-risk jurisdiction or the sender’s address matches a sanctions list, you must block it. If it’s a small transfer from a known, low-risk counterparty, you might proceed - but you still have to log why you made that call. Every decision must be documented.

And if a counterparty keeps failing to provide data? You must escalate. Report them. And if it keeps happening, you have to cut ties. The EU doesn’t want you to enable bad actors. It wants you to be the gatekeeper.

How Are Companies Actually Doing This?

There’s no manual. No simple checklist. So companies built tools. Platforms like KYCAID, Chainalysis, and Elliptic now offer compliance engines designed specifically for the EU’s zero-threshold rule. These systems do more than just store names and addresses. They:- Authenticate wallets using blockchain analytics

- Check for links to darknet markets or ransomware addresses

- Update sanctions lists in real time

- Support multiple data exchange protocols (like VASP-to-VASP messaging standards)

- Integrate with existing CRM and accounting software

Some exchanges in France and Germany have been doing this since 2022, because local regulators demanded it early. Now, the rest of the EU is catching up. The market for compliance tech has exploded. Vendors are competing to offer the fastest, most accurate, and least disruptive solutions. The ones that fail to scale will be left behind.

What About Cross-Border Transfers?

This is the biggest headache. The EU’s rule works perfectly within its borders. But crypto doesn’t care about borders. If you’re a German exchange sending funds to a U.S.-based wallet that doesn’t collect beneficiary data, you’re stuck. The U.S. doesn’t require that info for transfers under $3,000. So the German exchange has to treat that transaction as high-risk.The European Banking Authority says: treat any transfer to a non-compliant jurisdiction as high-risk. That means extra checks. Longer delays. More manual reviews. It slows things down. It frustrates users. And it costs money. Some firms are now refusing to send crypto to jurisdictions that don’t follow the EU’s rules. Others are building “compliance tunnels” - partnerships with compliant intermediaries in third countries to relay data properly.

Is This Even Fair?

Critics say yes - and no. On one hand, crypto has always been more private than banks. The EU is closing that gap. On the other, traditional finance handles billions in cash every day with far less oversight. A €5,000 cash deposit in a bank? No questions asked. A €5 crypto transfer? Full identity required.Some argue the zero threshold is overkill. The EU’s own data shows crypto-related crime is a tiny fraction of traditional finance crime. But regulators aren’t just reacting to crime. They’re trying to prevent it before it happens. And they’re sending a message: if you want to operate in the EU, you play by our rules. No exceptions.

What’s Next?

The EU isn’t done. This is just the start. In 2026, regulators will review whether the rule should extend to peer-to-peer transactions - meaning even wallet-to-wallet transfers might need data checks. They’re also looking at stablecoins, DeFi protocols, and NFT marketplaces. The goal? Total transparency.Meanwhile, other countries are watching. The UK, Canada, and Australia are all considering similar rules. Japan and South Korea are already tightening theirs. The EU didn’t just set a standard - it set the bar. And now, everyone else has to decide: do they follow, or risk being left out of the most regulated crypto market in the world?

What Happens If You Don’t Comply?

The consequences aren’t theoretical. In early 2025, a mid-sized crypto exchange in Spain was fined €2.3 million after regulators found it processed over 12,000 non-compliant transactions. The company had assumed small transfers didn’t matter. They were wrong. The fines didn’t just hurt their balance sheet - they lost partnerships with three major European banks. Their users started leaving. Within six months, they were sold to a compliant competitor.Smaller firms aren’t exempt. Even if you’re a startup with 500 users, if you’re registered in the EU, you’re bound by the same rules as Binance or Coinbase. There’s no small business exemption. No grace period anymore. The clock ran out on December 30, 2024.

Compliance isn’t a cost center. It’s your license to operate. Skip it, and you’re not just breaking the law - you’re cutting off your own air supply.

Does the EU Travel Rule apply to personal wallets?

No - not directly. The rule only applies when a transaction goes between two regulated crypto asset service providers (CASPs). If you send crypto from your personal wallet to another personal wallet, and neither side is a CASP, the rule doesn’t trigger. But if you use a regulated exchange to send funds to a wallet that’s held by a CASP (like a custodial wallet), then the rule applies. The key is whether a regulated entity is involved on either end.

What data must be shared under the EU Travel Rule?

For every transaction, the sending CASP must provide: the sender’s full name, account number or wallet identifier, and physical address. The receiving CASP must provide the beneficiary’s full name, account number or wallet identifier, and physical address. Missing any of these fields triggers a risk assessment. The data must be transmitted securely and stored for at least five years.

Can I still send crypto to someone outside the EU?

Yes - but it’s riskier. If the recipient’s provider doesn’t comply with EU rules, your exchange must treat the transaction as high-risk. You may need to manually review it, delay it, or even block it. Some exchanges now refuse to send crypto to jurisdictions that don’t have Travel Rule compliance. It’s not illegal to send it, but it’s legally risky for your provider to process it.

Are there any exemptions for small transactions?

No. The EU has no de minimis threshold. Even a €0.01 transfer between two regulated CASPs requires full data exchange. This is the defining feature of the EU’s approach - it’s universal. There are no exceptions based on amount, frequency, or purpose.

How do I know if my crypto provider is compliant?

Check if they’re registered with a national financial authority in an EU member state - like BaFin in Germany, ACPR in France, or the FCA in the UK (for UK-based firms serving EU clients). Regulated providers must publicly state their compliance status. If they don’t mention MiCA or Travel Rule compliance, assume they’re not ready. Don’t use them for transfers unless you’re willing to risk delays or account freezes.

Sara Lindsey

November 14, 2025 AT 22:08Anthony Forsythe

November 16, 2025 AT 00:23The EU didn't just implement a regulation - they declared war on anonymity itself. This isn't about crime prevention, it's about control. They want every digital movement tracked, logged, and cataloged under the banner of 'security.' But security without liberty is just surveillance with better PR. The moment we accept that a €0.01 transfer requires a passport, we've surrendered the soul of decentralized finance. The blockchain was meant to be a refuge from this kind of bureaucratic overreach - not a digital cage with KYC bars.

And let’s be honest - if you're going to treat a coffee payment like a money laundering scheme, why not just ban crypto altogether? At least then we'd know where we stand. But no, they want the illusion of freedom while pulling every string. The irony? The real criminals - the ones moving billions in cash, shell companies, and offshore accounts - don't even use crypto. They're laughing at us while we fight over whether our wallet address needs a notary stamp.

This rule doesn't make the system safer. It just makes it slower, more expensive, and less accessible. It punishes the honest, the small, the everyday user - the very people crypto was supposed to empower. And for what? A few hundred cases of minor fraud that banks could’ve caught with one eye closed? The EU isn't regulating crypto - it's burying it under paperwork.

And now the world watches. The UK, Canada, Australia - they're all nervously adjusting their ties, wondering if they should join the parade of digital handcuffs. But here's the truth: compliance isn't innovation. It's surrender. And if we keep bowing to these demands, we won't just lose privacy - we'll lose the reason crypto ever mattered in the first place.

alex piner

November 17, 2025 AT 04:20Gavin Jones

November 17, 2025 AT 14:38While I appreciate the intent behind enhanced financial transparency, the zero-threshold implementation of the EU Travel Rule presents a profound operational paradox. The regulatory architecture assumes perfect interoperability across global jurisdictions, yet the reality is that over 80% of crypto service providers outside the EU remain non-compliant. This creates a systemic friction point wherein legitimate, low-risk transactions are arbitrarily suspended due to the absence of data from counterparties operating under entirely different legal paradigms. The consequence is not enhanced security, but rather the fragmentation of the global crypto ecosystem into isolated regulatory enclaves.

Furthermore, the burden of real-time identity verification and data exchange imposes disproportionate costs on small and medium-sized CASPs, effectively consolidating market power into the hands of a few large incumbents who can afford the compliance infrastructure. This is regulatory capture disguised as consumer protection. The EU has succeeded in creating a fortress - but at the cost of turning its own market into a walled garden, isolated from the broader innovation occurring elsewhere.

It is not merely a question of compliance - it is a question of whether centralized oversight is compatible with the foundational ethos of decentralization. Perhaps the more prudent path would have been to mandate data exchange only for transactions above a nominal threshold, while deploying AI-driven anomaly detection for higher-risk flows. Instead, we have chosen uniformity over intelligence, and bureaucracy over adaptability.

Mauricio Picirillo

November 18, 2025 AT 18:42Liz Watson

November 19, 2025 AT 14:57Oh wow. The EU finally figured out that people use crypto to avoid banks. And their solution? Make crypto *more* like banks. Brilliant. Truly. Who needs privacy when you can have paperwork? I’m sure the 14-year-old who sent €0.50 to their Discord streamer is now being investigated by Europol. Next up: mandatory ID scans for Bitcoin ATMs. And don’t forget - you’ll need to submit a notarized letter explaining why you bought Dogecoin.

Let’s be real. This isn’t about crime. It’s about control. The EU doesn’t trust its citizens with money. They trust spreadsheets. And if you’re not screaming about this, you’re not paying attention.

Rachel Anderson

November 20, 2025 AT 06:11This isn't regulation. It's a digital autocracy. They didn't just remove the threshold - they removed the soul of crypto. Every transaction now carries the weight of state surveillance. You think you're sending €1 to a friend? No. You're submitting a dossier. You're handing over your digital fingerprints to a bureaucracy that doesn't care if you're innocent - only if you're traceable.

The irony? The people who actually launder money don't use regulated exchanges. They use mixers. They use privacy coins. They use offshore OTC desks. The EU didn't stop criminals. They just made it harder for normal people to send money to their cousins in Nigeria or tip their favorite artist on Twitter. This isn't progress. It's a dystopian performance art piece called 'The Death of Decentralization.'

And the worst part? We're all just supposed to nod and say 'thank you for protecting us.' Meanwhile, banks move billions in cash with zero oversight. But a €0.01 crypto transfer? Full identity verification. Required. Non-negotiable. The hypocrisy is breathtaking.

Hamish Britton

November 20, 2025 AT 17:50Byron Kelleher

November 21, 2025 AT 07:36Cherbey Gift

November 21, 2025 AT 15:14Let me tell you something - this ain’t regulation, this is cultural imperialism. The EU thinks their way is the only way. But in Lagos, in Accra, in Nairobi - people use crypto because banks are broken, because ATMs don’t work, because your salary gets delayed for months. And now? Now you gotta give your full name, your address, your mother’s maiden name just to send 500 naira to your auntie for market money? What kind of madness is this?

You think you’re fighting crime? You’re killing survival. You’re criminalizing the poor. The rich still move money through shell companies and private jets. But the girl who sells phone credit on WhatsApp? She’s the one who gets locked out. That’s not justice. That’s arrogance dressed in compliance.

And don’t give me that ‘global standard’ nonsense. The U.S. has a $3,000 threshold. Why? Because they know not everyone lives in a five-star hotel with a Swiss bank account. The EU doesn’t care. They want the world to kneel. And we’re supposed to thank them for the chains?

When your rule makes it harder for a mother in Port Harcourt to send money to her child than it is for a hedge fund to launder billions - you’re not protecting the system. You’re protecting your ego.

Kandice Dondona

November 23, 2025 AT 14:48Becky Shea Cafouros

November 23, 2025 AT 19:51Drew Monrad

November 23, 2025 AT 22:18Oh great. So now the EU is the world’s most aggressive tax collector with a blockchain fetish. Let me guess - next they’ll require a notarized affidavit every time you send ETH to your cousin’s NFT project. And if you don’t? You’re a terrorist. Or worse - a tax evader.

Let’s be real: this rule doesn’t stop crime. It just makes crypto less fun. And that’s the goal. The banks are terrified. They see crypto as the future - and they’re fighting back with paperwork. This isn’t regulation. It’s sabotage disguised as safety.

And don’t tell me ‘it’s for the children.’ The children aren’t sending crypto. The adults are. And the adults just want to move money without filling out ten forms. So why not just fix the system instead of crushing it under bureaucracy?

Next stop: mandatory emotional stability certificates for crypto traders. Because clearly, if you’re using Bitcoin, you must be unstable.

Cody Leach

November 24, 2025 AT 15:35sandeep honey

November 25, 2025 AT 09:59Mandy Hunt

November 27, 2025 AT 09:41anthony silva

November 29, 2025 AT 09:19David Cameron

November 30, 2025 AT 05:06What we're witnessing isn't a regulatory shift - it's a philosophical surrender. The blockchain was conceived as a mechanism to bypass intermediaries, to enable direct, trustless value transfer. The EU’s zero-threshold rule doesn’t enhance security - it re-establishes the very intermediaries crypto was designed to dismantle.

The question isn't whether this rule prevents crime. It's whether the cost of compliance erodes the core value proposition of decentralized finance. If every transaction requires identity verification, then what distinguishes crypto from a digital bank account? The answer: nothing. We’ve traded decentralization for bureaucracy. We’ve traded freedom for friction.

And yet - we are complicit. We built the tools. We praised the anonymity. And now we're surprised when the state demands its due. Perhaps the real failure isn’t the regulation - it’s our collective amnesia about why we started this journey in the first place.

Robert Astel

December 2, 2025 AT 00:42Okay so i read this whole thing and honestly i'm kinda shook. i thought crypto was supposed to be free and easy but now i feel like every time i send money i'm being watched by some government drone with a clipboard. i mean i get the fraud thing but like... i sent my sister 1 euro for her birthday last week. did they log that? do they have my address now? what if i want to send 10 cents to a guy who made a funny meme? do i need to file a form? i just wanted to be nice.

and dont even get me started on the people in other countries. like in africa or india, people use crypto because their banks are trash. now they gotta jump through the same hoops as a german bank? that's not fair. that's not helping. that's just making life harder for people who need it the most.

and why does the eu think they get to decide how the whole world should do crypto? the us has a $3k limit. japan's chill. but the eu? nope. every cent. every time. even if you're buying a digital cat picture. i feel like this is less about crime and more about control. and i'm not sure i want to live in a world where sending money is a legal audit.

also... who's paying for all this? the little exchanges? the startups? they're gonna go under. and then only the big players survive. so now we're back to the same system we wanted to escape. ironic, right?