How Crypto Exchanges Implement AML: KYC, Monitoring, and Compliance Systems

Mar, 16 2026

Mar, 16 2026

When you trade Bitcoin or swap Ethereum on a crypto exchange, you might think it’s just you and the blockchain. But behind the scenes, a complex system is working to stop criminals from turning stolen money into clean crypto. This system is called AML-Anti-Money Laundering. It’s not optional. It’s the law. And every major exchange has to follow it, or face massive fines, shutdowns, or even jail time for its founders.

Why AML Matters in Crypto

Crypto wasn’t built to hide crime. But its pseudonymous nature made it a target. Before 2019, many exchanges operated like the wild west-no ID checks, no transaction tracking, no oversight. That changed when U.S. regulators-FinCEN, the SEC, and the CFTC-declared that crypto exchanges are financial institutions under the Bank Secrecy Act. Suddenly, they had to follow the same rules as banks. The Financial Action Task Force (FATF), the global standard-setter for AML, gave exchanges three clear tasks: Know Your Customer, monitor transactions, and report bad activity. Get any one wrong, and you’re at risk.Know Your Customer (KYC): The First Line of Defense

KYC isn’t just asking for your email. It’s verifying who you are, where you’re from, and whether you’re allowed to use the platform. Exchanges collect:- Full legal name

- Government-issued ID (passport, driver’s license)

- Proof of address (utility bill, bank statement)

- Selfie or video for liveness detection

- Sanctions lists (like OFAC’s)

- Politically Exposed Persons (PEPs)-government officials with higher corruption risk

- Adverse media-news about you linked to fraud, drugs, or terrorism

Transaction Monitoring: Watching Every Move

Once you’re in, the system doesn’t stop watching. Every crypto transaction you make gets analyzed in real time. Exchanges don’t just look at your balance-they track patterns. Here’s how:- Amount thresholds: If you suddenly send $50,000 to 10 different wallets, that’s a red flag.

- Frequency spikes: Sending 50 small transfers in one hour? Suspicious.

- Destination analysis: Does your money go to mixers, tumblers, or addresses linked to past hacks?

- Behavioral baselines: If you usually trade $100 a week and suddenly move $10,000, the system asks: “Why?”

Two Approaches: Allow Lists vs. Deny Lists

There are two main ways exchanges handle wallet addresses:- Deny lists: Block transactions from or to known bad addresses. This is common. If a wallet was linked to the BitMart hack in 2022, it’s on the list. Any coin touching it gets flagged.

- Allow lists: Only allow transactions between wallets that passed KYC. This is stricter-and rare. Only a few regulated exchanges use it. It’s like a bank account: only you and approved contacts can send money in or out.

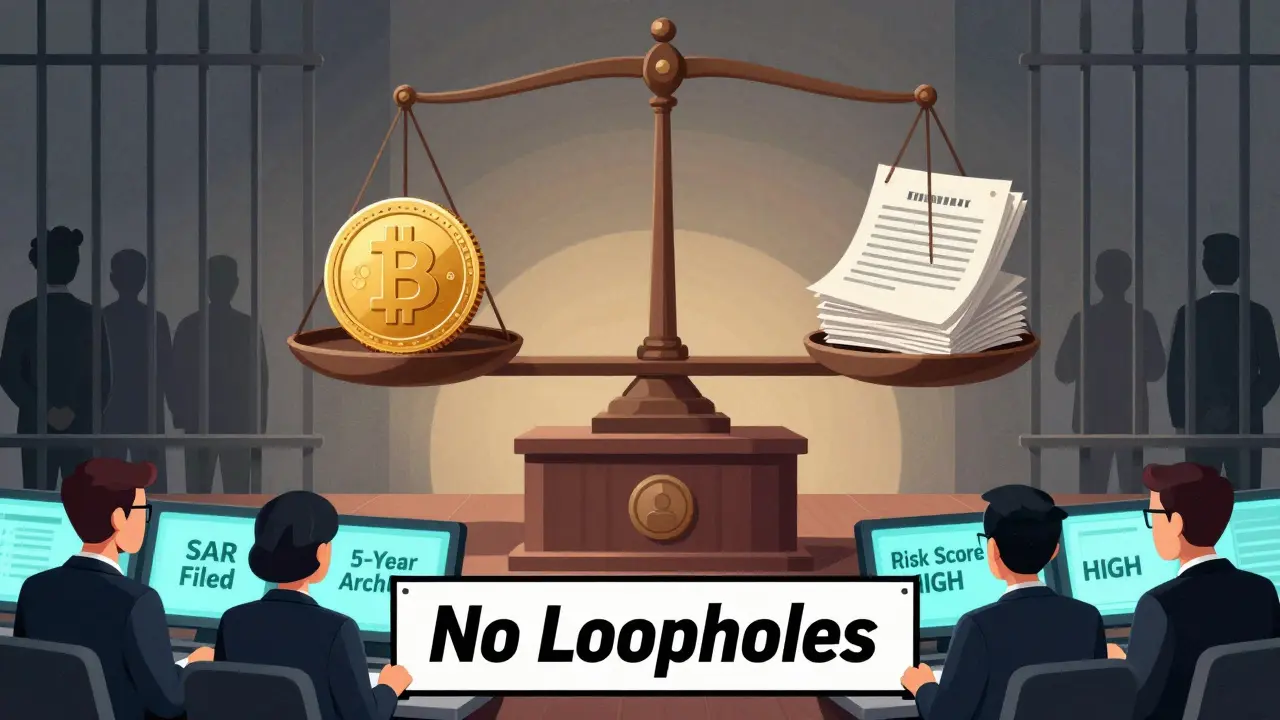

Reporting and Response: When Something Goes Wrong

If the system flags something, it doesn’t just sit there. It triggers a response:- Customer is contacted: “Why did you send this money?”

- Account is frozen: Funds are held while investigators review.

- Report is filed: Suspicious Activity Reports (SARs) go to FinCEN or local regulators.

- Records are kept: All logs, emails, transaction history are archived for 5-7 years.

Global Rules, Local Problems

AML isn’t the same everywhere. The EU’s 5AMLD requires exchanges to collect more data than the U.S. does. In Singapore, you need a license. In Japan, you need to report every transaction over $10,000. In the U.S., you report anything over $10,000 and file SARs for anything suspicious-even if it’s $500. That means global exchanges like Binance or Coinbase have to run dozens of compliance engines at once. One for the U.S., one for the EU, one for the UK, one for Singapore. Each has different rules, different reporting deadlines, different definitions of “suspicious.” They hire teams of lawyers, data scientists, and compliance officers just to keep up. And they train them monthly. Because the rules change constantly.Technology That Makes It Work

You can’t do this manually. You need software:- APIs: Connect to global sanctions databases in real time.

- Low-code platforms: Let compliance teams tweak rules without coding.

- Risk scoring: Assign each user a risk level-low, medium, high-based on location, transaction history, and ID verification.

- Blockchain analytics: Tools like Chainalysis and Elliptic trace coin flows across thousands of wallets.

What Happens When AML Fails?

The penalties are brutal. - In 2021, a derivatives exchange paid $100 million to settle AML violations.- Three founders of a crypto firm pleaded guilty and each paid $10 million in fines to avoid prison.

- In 2023, a major exchange was banned from operating in Canada because it failed to report suspicious activity for two years. These aren’t warnings. They’re wake-up calls. Exchanges that cut corners don’t survive. They get shut down, fined, or taken over.

The Future: More AI, Less Human Error

The next leap is in automation. Exchanges are moving from rule-based systems to AI that learns. Instead of saying “block if over $5,000,” the system learns: “This user normally sends $200 every Friday. This $4,800 transfer to a new wallet on a Tuesday? That’s odd.” Biometrics are getting better too. Voice recognition, facial mapping, even typing rhythm analysis to confirm it’s really you. And regulators? They’re catching up. The EU is pushing for a unified crypto AML rulebook. The U.S. is considering mandatory blockchain analytics for all exchanges. The goal? No more loopholes.Bottom Line

Crypto exchanges don’t implement AML because they want to. They do it because they have to. It’s not about privacy. It’s about survival. The systems are complex, expensive, and constantly evolving. But they work. Millions of daily transactions pass through them without triggering alarms. That’s because they’re built to catch the bad ones-before they turn crypto into cash.For users, it means more ID checks. Slower deposits. More questions. For the industry, it means legitimacy. The future of crypto isn’t anonymous. It’s accountable.

Do all crypto exchanges have to follow AML rules?

Yes-if they operate in regulated markets like the U.S., EU, UK, Japan, or Singapore. Exchanges that don’t follow AML rules can’t legally accept users from those regions. Some unregulated exchanges exist, but they’re risky to use and often get blocked by banks and payment processors.

Can I avoid KYC on a crypto exchange?

On regulated exchanges, no. If you try to skip KYC, you won’t be able to deposit, trade, or withdraw. Some decentralized exchanges (DEXs) like Uniswap don’t require KYC, but they don’t offer fiat on-ramps either. To convert crypto to dollars, you’ll need a regulated exchange-and that means KYC.

What happens if my transaction gets flagged?

Your account will likely be frozen. The exchange will contact you to explain the transaction. If you provide a legitimate reason (like receiving a salary or selling property), they may lift the freeze. If not, they’ll file a Suspicious Activity Report (SAR) with authorities and may permanently restrict your account.

Do AML systems track my private wallet?

Only if you send funds to or from a regulated exchange. Once crypto leaves the exchange and goes to your personal wallet, the exchange can’t track it. But if you later send that same crypto back to the exchange, they’ll analyze its history. If it passed through a flagged wallet before, you might get questioned.

Why do some exchanges block certain countries?

Some countries are under international sanctions, or have weak AML laws. Exchanges block users from those places to avoid regulatory risk. For example, many exchanges block users from Iran, North Korea, or Syria because U.S. and EU rules prohibit doing business there. It’s not about politics-it’s about legal survival.

Robert Kunze

March 17, 2026 AT 20:25Graham Smith

March 18, 2026 AT 11:24Jerry Panson

March 19, 2026 AT 17:49Katrina Smith

March 20, 2026 AT 17:08Anastasia Danavath

March 21, 2026 AT 17:00anshika garg

March 23, 2026 AT 09:23Bruce Doucette

March 24, 2026 AT 18:37Marie Vernon

March 26, 2026 AT 11:06Billy Karna

March 27, 2026 AT 18:05Patty Atima

March 28, 2026 AT 18:30Ernestine La Baronne Orange

March 29, 2026 AT 22:44sai nikhil

March 30, 2026 AT 02:39Diane Overwise

March 30, 2026 AT 06:05rajan gupta

March 30, 2026 AT 20:59Cheri Farnsworth

April 1, 2026 AT 03:15Gene Inoue

April 2, 2026 AT 15:07Ricky Fairlamb

April 3, 2026 AT 04:58Arlene Miles

April 4, 2026 AT 00:56Jessica Beadle

April 4, 2026 AT 04:32